We were not the least bit surprised to see Specialized take the plunge. Mike Sinyard was raised in the NoCal-Silicon Valley-hood and he has admired the likes of Jobs and other tech executives for decades. He is extremely competitive and when one of his many x-leaders joined the Canyon USA leadership team he studied them, watched them, and has been building a strong digital marketing team for years in preparation. As Canyon grew, got sold for a Tesla like price to a European Private-Equity firm touting years of 50% plus Tesla-like growth, it was only a matter of time until Specialized joined the fray.

Now the only cards left to play are what will the other Super 10 players do in response? Schwinn and GT have been selling DTC for over a year. It is anyone’s guess what Cannondale will do, though it has been effectively selling DTC via REI for quite some time. Pon’s other premium brands, Santa Cruz and Cervelo, have been sold DTC by the #2 cycling player in the USA, namely Backcountry.com. Canyon of course was founded as a DTC only player and has steadily moved up the intend to buy ranks as per VeloNews, Pinkbike, VitalMTB, and Enduro-MTB.com consumer research. Now all eyes will be on Trek, and John Burke has the lead on the purchase of company owned stores so he could be viewed as already selling Direct via his many, many company owned stores.

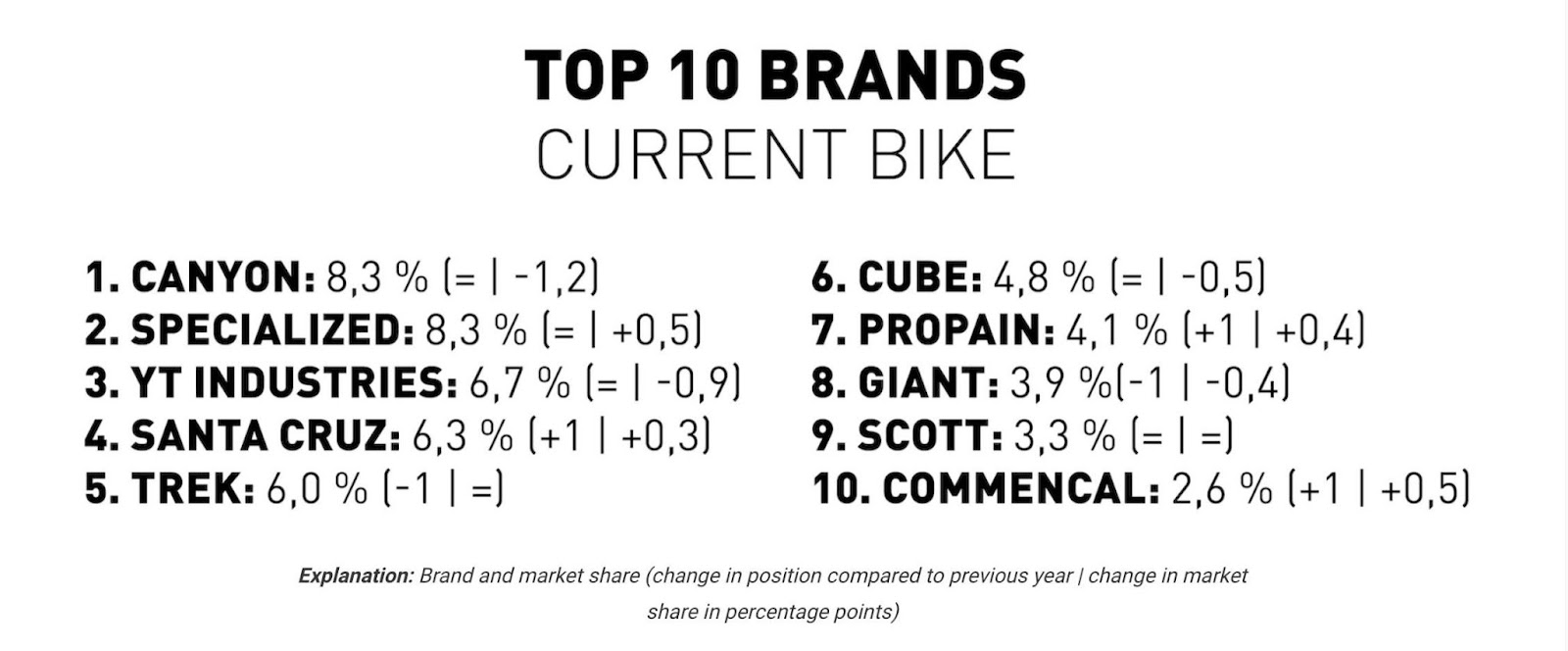

After my quick CEO cycling check ins this past week, it seems most of the other Top 50 cycling bike brands will prepare and likely roll out a DTC play by year-end. Viewing the chart above 6 of the 10 are either DTC only, or OMNI channel brands as of this moment.

WHAT HAPPENED IN 2021?

For our brand partners in outdoor-bike-ski, 2021 was another record smashing year! The only ones lagging were brands with supply chain issues. For those with a strong supply chain, it was another record year with high growth. The overall DTC market grew around 16%. While a slower pace than the closed store environment of COVID stricken 2020, it was still outstanding! By most measures, not including gas, groceries, etc., brands are realizing about 20%+ of their US sales or higher via DTC web stores, and those with excellent Amazon channels are pushing twice that percentage.

WHERE DO WE GO FROM HERE?

We believe all brands will sell DTC by the end of 2022. We expect DTC sales growth of ~15% and certainly we will welcome the return of full in-store shopping in Q2 2022 as COVID stress subsides. Brands need to have an “owned media” strategy so they can nurture, feed, and monetize for Lifetime Customer Value. If your brand is not managing an effective digital marketing funnel and checkout, you are leaving money on the table. You also risk the possibility that the consumer will change their mind either because of supply, other competitors, or impulse, thus leaving your brand with lower sales than the Omni-Present brands with effective strategies to close the deal regardless of the channel. In the end they might have your product shipped to their home, buy it on Amazon, or go to the store, but premium brands need sales to fuel increased investments in RND, staff and marketing.

Think + Crank,

Scott Montgomery